{kind=link}

I’d argue for moderation.

I often have a powerful opinion on points in my sphere, however have been going backwards and forwards about one element prone to be in any bundle to repair Social Safety – specifically, rising the taxable wage base. Some enhance within the wage base is nearly inevitable as a result of rising wage inequality has prompted the share of wages topic to taxation to say no sharply for the reason that final main piece of laws in 1983 (see Determine 1).

The minimalist possibility is solely to lift the taxable restrict from $168,600 in 2024 to an quantity that might be sure that 90 p.c of wages had been topic to the payroll tax – roughly $300,000. Probably the most aggressive possibility can be to take the restrict off altogether and provide no further advantages. In between are choices that take away the restrict and provide advantages of assorted generosity.

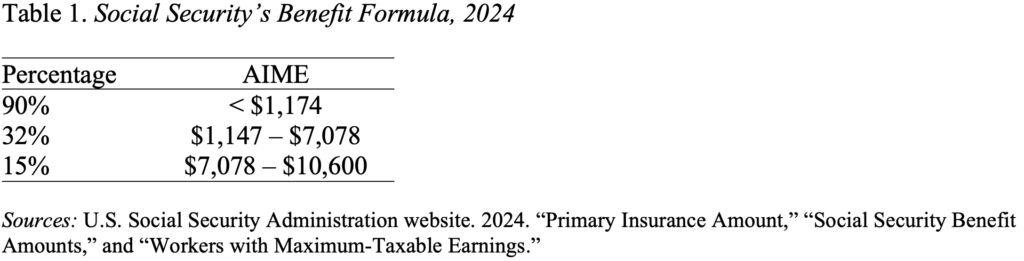

As background, it’s useful to know how advantages are at present calculated. Step one is to calculate the employee’s common listed month-to-month earnings (AIME), which entails adjusting the employee’s wage historical past for will increase within the normal wage degree, choosing the best 35 years, and taking the month-to-month common. The second step is to use the profit components (see Desk 1) to calculate the employee’s main insurance coverage quantity. (The odds within the profit components are fastened by regulation, however the greenback ‘bend points’ are adjusted every year for modifications within the nationwide common wage index.) Lastly, the first insurance coverage quantity is adjusted actuarially for early or late claiming.

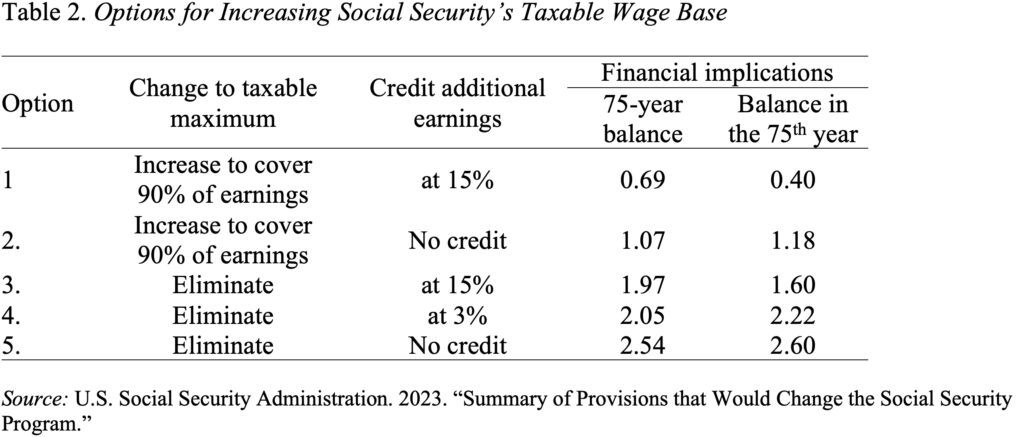

The Social Safety actuaries put out a beautiful booklet that comprises greater than 150 choices for closing the 75-year deficit by both reducing advantages or elevating further income. Desk 2 summarizes 5 of the 19 choices for rising the taxable wage base. For context, the 2024 Trustees Report projected Social Safety’s shortfall over the following 75 years to be 3.50 p.c of taxable payrolls.

Clearly, the most important monetary acquire comes from eliminating the taxable most – Choices, 3,4 and 5. I don’t like Choice 5 as a result of it dissolves any hyperlink between payroll tax contributions and advantages, which in the long term may undermine assist for this system. Choice 3 appears too beneficiant to excessive earners, and the positive aspects to Social Safety would decline over time as persistent wage inequality results in speedy development in advantages among the many excessive earners. Due to this fact, the selection to me comes all the way down to elevating the cap to cowl 90 p.c of earnings or eliminating the cap and including a 3-percent bracket to the profit components (Choice 4).

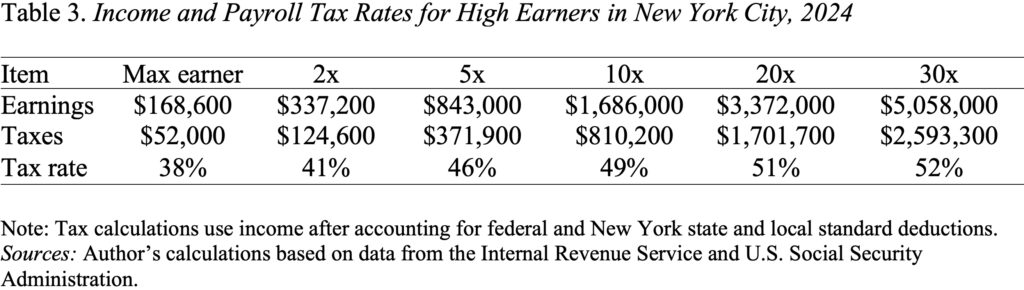

The selection then comes all the way down to how far more can we wish to tax excessive earners. My colleague Ray Madoff on the Boston School Regulation Faculty makes a convincing case that top earners – that’s, individuals who get all their earnings within the type of wages and salaries – pay their full share of taxes. Certainly, a fast calculation for these dwelling in New York Metropolis suggests that actually excessive earners pay greater than half their compensation in earnings (federal, state, and metropolis) and payroll taxes (no taxable most on the Medicare tax plus a 0.9-percent tax on earnings above $200,000 for singles and $250,000 for married {couples}) (see Desk 3). I do know New York is on the excessive aspect when it comes to taxes, however that’s the place I get most of my complaints from!

In the long run, some mixture of Choices 1 and a pair of looks as if the way in which to go – increase the taxable wage base to cowl 90 p.c of earnings and credit score a small proportion (maybe 3 p.c) of the earnings in the direction of advantages. The large choice for me was not taking the cap off altogether. Thanks for serving to me work via my dilemma.