{kind=link}

Picture supply: easyJet plc

As an easyJet shareholder, the corporate’s future issues to me. And presently, it’s not wanting nice. The share value is down 47% in 5 years, having underperformed the FTSE 100 for the previous three years.

Not that I’m contemplating promoting my shares. Relatively, I’m questioning if now is an effective time to purchase extra, subsequently lowering my common spend per share.

First, I need to attempt to determine the place the shares are headed.

To take action, I’ve studied some key metrics which are used to forecast progress potential. Typical progress fee metrics embody:

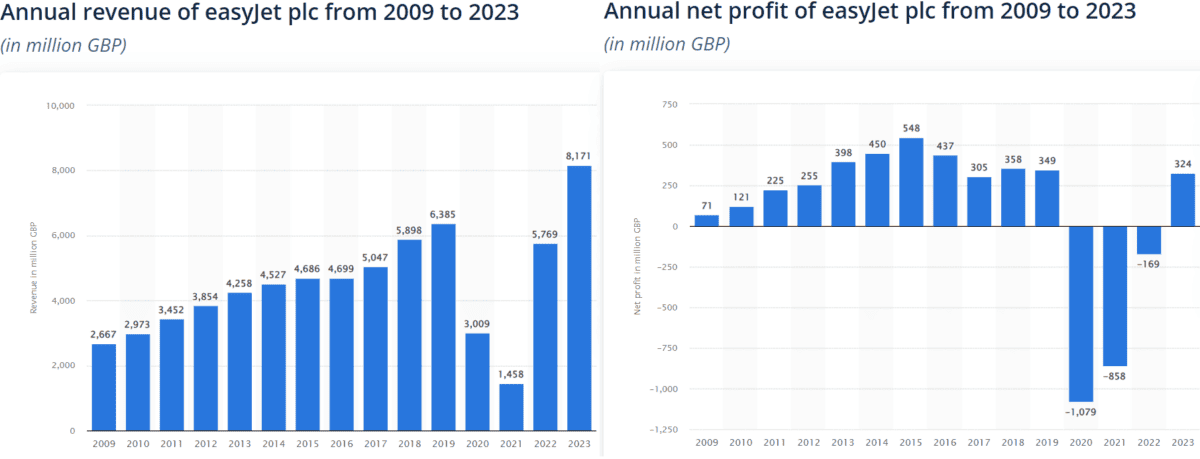

Income and earnings

Income is the full earnings an organization generates, whereas earnings are the revenue remaining after bills, taxes and different prices.

Airways have been among the many worst affected companies throughout the pandemic and like many others, easyJet is but to get well totally. It turned worthwhile once more this yr, with earnings of £324m — barely down over 5 years. However an analogous occasion may render it unprofitable once more, digging it even additional into debt.

For now, income stays excessive, at £8.17bn.

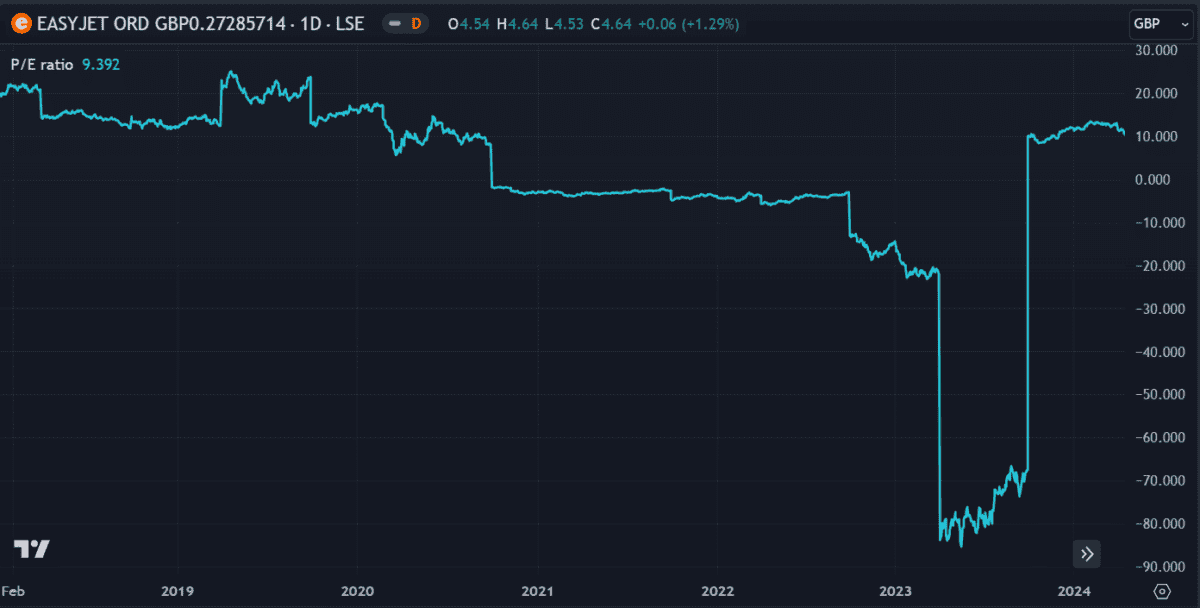

P/E ratio

easyJet’s P/E ratio appears low at 9.3, contemplating the UK market common is round 16.5. However price range journey is a fiercely aggressive business in Europe and easyJet faces stiff competitors from rivals Ryanair, Wizz Air and Jet2. At the moment, its P/E ratio is greater than Jet2 and Wizz Air.

On one hand, this might point out that traders have greater confidence within the airline. Nevertheless it additionally reduces its comparative progress potential. Nevertheless, with earnings forecast to develop by 33%, its ahead P/E ratio may drop to 7 within the coming 12 months.

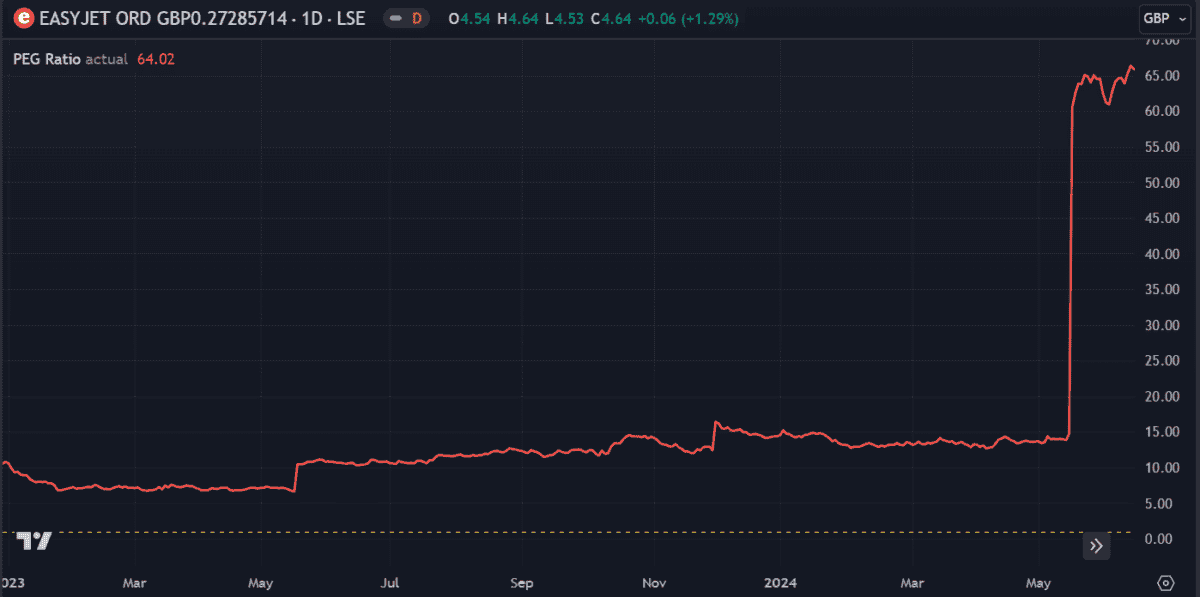

PEG ratio

The PEG ratio compares the value to anticipated earnings progress to gauge what sort of returns an investor may anticipate. If this metric is 1 (or 100%), earnings and value are anticipated to extend equally. Any quantity under 1 is sweet, as the value is anticipated to outperform earnings.

easyJet presently has PEG ratio of 0.64 (displayed on the chart as 64%). However its progress is threatened by any hiccup within the native economic system that may trigger shoppers to chop down on pointless bills.

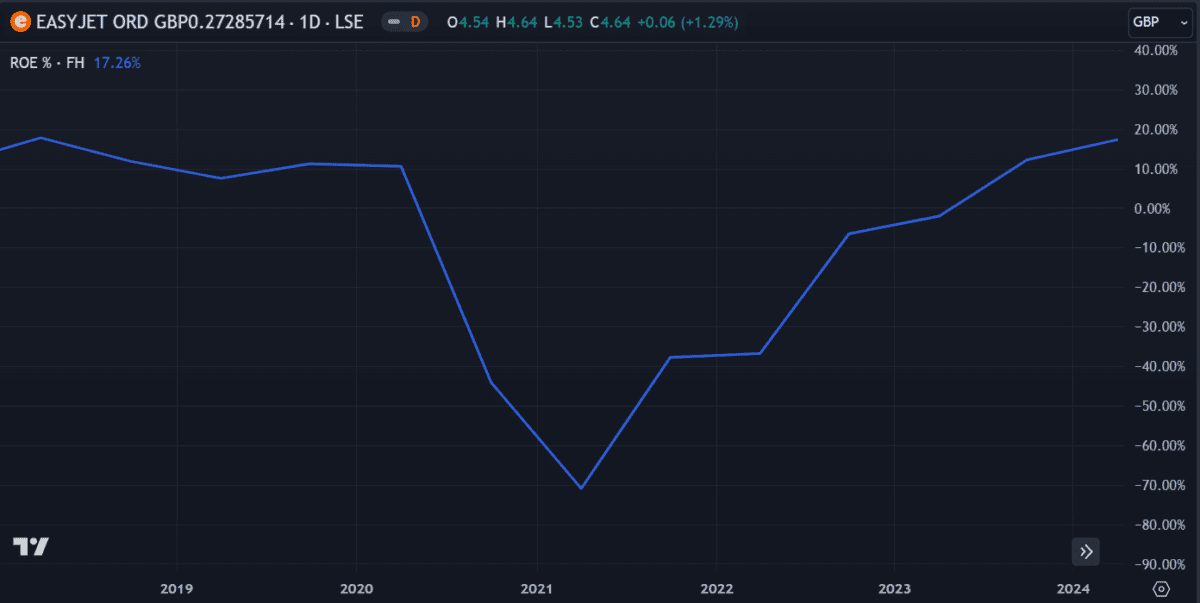

ROE

ROE is a measure of an organization’s monetary efficiency, calculated by dividing web earnings by shareholders’ fairness. easyJet’s ROE has lately climbed again as much as pre-Covid ranges round 17%.

Whereas the advance is spectacular, it stays significantly decrease than the business common of 30%. Hopefully, its progress will proceed, prompting the share value to comply with swimsuit.

The underside line

A number of metrics in these charts point out progress potential. In the newest quarterly earnings report, passenger numbers rose 8% and income elevated 16%. This was boosted by progress within the airline’s new ‘holidays’ providing, which has proved standard.

On the similar time, the share value continues to wrestle and the inventory carries a number of dangers. I purchased EZJ shares when air journey reopened because it appeared essentially the most promising UK airline inventory on the time.

Up to now, I’m dissatisfied within the efficiency and never impressed to purchase extra. However with no airline providing something extra promising, I’ll maintain my shares for now and see the place it goes.