{kind=link}

Trustees Report continues to point out 75-year deficits and exhaustion of belief fund in early 2030s.

The 2024 Social Safety Trustees Report repeats the drumbeat that the Social Safety program faces a deficit equal to three.50 % of payroll over the following 75 years and that its belief fund is scheduled for exhaustion within the early 2030s.

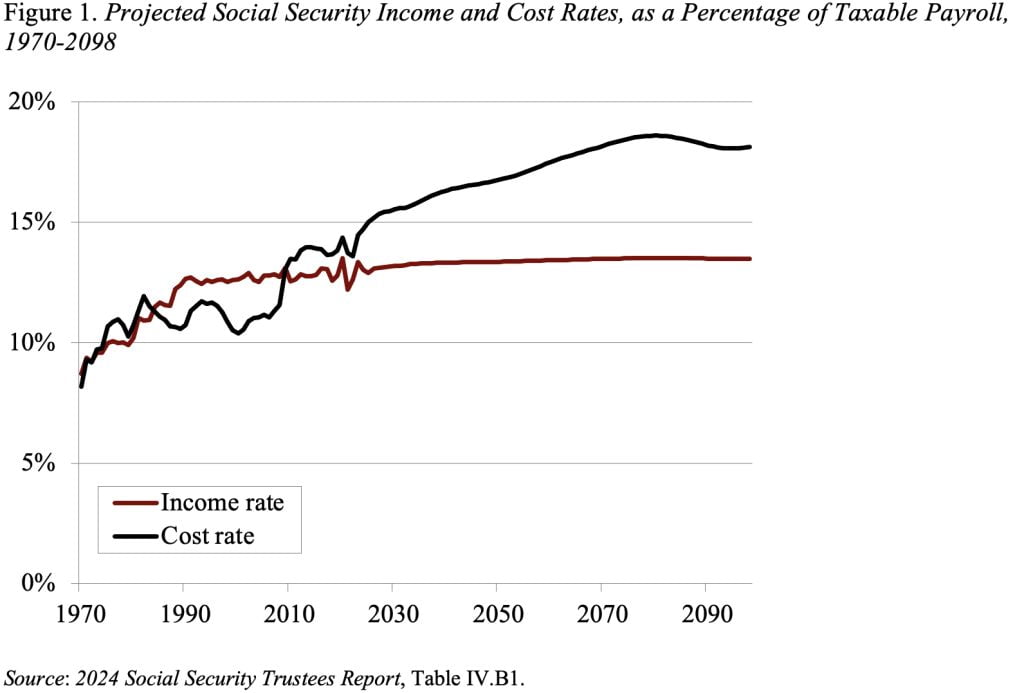

The 75-year deficit is the results of a relentless tax price and rising prices. The rise in prices is pushed by the demographics, particularly the drop within the whole fertility price after the Child-Increase interval. The mixed results of a slow-growing labor drive and the retirement of Boomers cut back the ratio of employees to retirees from 3:1 to 2:1 and lift prices commensurately (see Determine 1).

The 75-year deficit is the distinction between the present discounted worth of scheduled advantages and the current discounted worth of future taxes plus the property within the belief fund. This calculation exhibits that Social Safety’s long-run deficit is projected to equal 3.50 % of coated payroll earnings. That determine implies that if payroll taxes had been raised instantly by 3.50 proportion factors – 1.75 proportion factors every for the worker and the employer – the federal government would be capable to pay the present bundle of advantages for everybody who reaches retirement age by 2098, with a one-year reserve on the finish.

The 75-year money stream deficit is mitigated somewhat by the existence of a belief fund, with property currently equal to roughly two years of advantages. These property are the results of money stream surpluses that started in response to reforms enacted in 1983. The retirement (OASI) belief fund is projected to be depleted in 2033. Sure, the Incapacity Insurance coverage (DI) belief fund has sufficient to pay advantages for the total 75-year interval, so the date of depletion for the mixed OASDI belief funds has moved again a 12 months to 2035. However combining the 2 programs would require a change within the regulation; therefore, underneath present regulation the action-forcing date is 2033 – 9 years from now.

It’s essential to emphasise that the depletion of the belief fund doesn’t imply that OASI is “bankrupt.” On the time of depletion, payroll tax revenues preserve rolling in and may cowl 79 % of at the moment legislated advantages. (If the OASI and DI belief funds had been merged, the protection numbers can be 83 %.) Relying solely on present tax revenues, nevertheless, implies that advantages can be lower about 20 % for each present retirees and future beneficiaries

The underside line is that we’re going to should both provide you with extra money or lower Social Safety advantages within the 2030s. My view is that we must always enhance revenues and keep advantages. That view is predicated on the wobbly state of the remainder of our retirement system: 1) solely about half of people within the personal sector, at any second in time, work for an employer with a retirement plan; and a pair of) for many of these fortunate sufficient to have a plan, their 401(okay)/IRA holdings are modest.

Fixing Social Safety isn’t an enormous deal. The shortfall equals just one % of GDP, and the adjustments required are properly inside the bounds of fluctuations of different applications. Doing it sooner quite than later would preserve extra choices open, distribute the burden extra equitably throughout cohorts, and most significantly, restore confidence within the nation’s main retirement program.