{kind=link}

The present index is an effective compromise.

It’s “Social Security COLA-speculation” season, and with it comes the annual controversy about whether or not the federal government is utilizing the proper index to regulate advantages. I might argue that the present index is nice sufficient; it could simply be considered as a compromise between the 2 main options – the CPI-E, which displays the spending of the older inhabitants and rises sooner, and the Chained CPI, which permits for extra substitution and rises extra slowly.

The federal government presently adjusts Social Safety advantages to maintain tempo with the Client Value Index for City Wage Earners and Clerical Staff (CPI-W). This index, which covers about 29 % of the inhabitants, was the one one obtainable when the Social Safety COLA was first launched in 1972. In 1978, the Bureau of Labor Statistics expanded the pattern to all city residents and created the CPI-U, which covers about 93 % of the inhabitants, together with most retirees. Regardless of the broader protection and the prominence given the CPI-U within the month-to-month inflation report, the federal government has stayed with the CPI-W for the Social Safety COLA – almost certainly as a result of the 2 indices observe one another very carefully.

For many years critics have argued that the bundle of products within the CPI-W doesn’t signify the spending patterns of retirees and subsequently understates the inflation truly skilled by older Individuals. Extra particularly, older folks spend extra on well being care than the younger and well being care costs usually rise sooner than different items, so the CPI-W understates the rise in the price of dwelling for retirees. In response, in 1988, the BLS launched the CPI-E, which displays the spending patterns of individuals 62 and over.

Economists, then again, argue that the present CPI overstates inflation, as a result of it doesn’t account for a way folks change their shopping for habits in response to a value improve. The idea is that by shifting to a detailed substitute services or products, folks can reduce the rise of their value of dwelling and be simply as completely happy. Since January 1999, a geometrical imply system has allowed for modest substitution throughout the 211 merchandise classes (which, mixed with 38 geographic areas, complete 8,018 fundamental indexes). However it didn’t enable for substitution throughout merchandise classes, equivalent to pork and beef. The “chained CPI” displays shifts in shopping for patterns that happen when the value of pork rises and the value of beef doesn’t. In 2018, Congress completely switched the inflation adjustment for federal earnings tax provisions to the chained CPI.

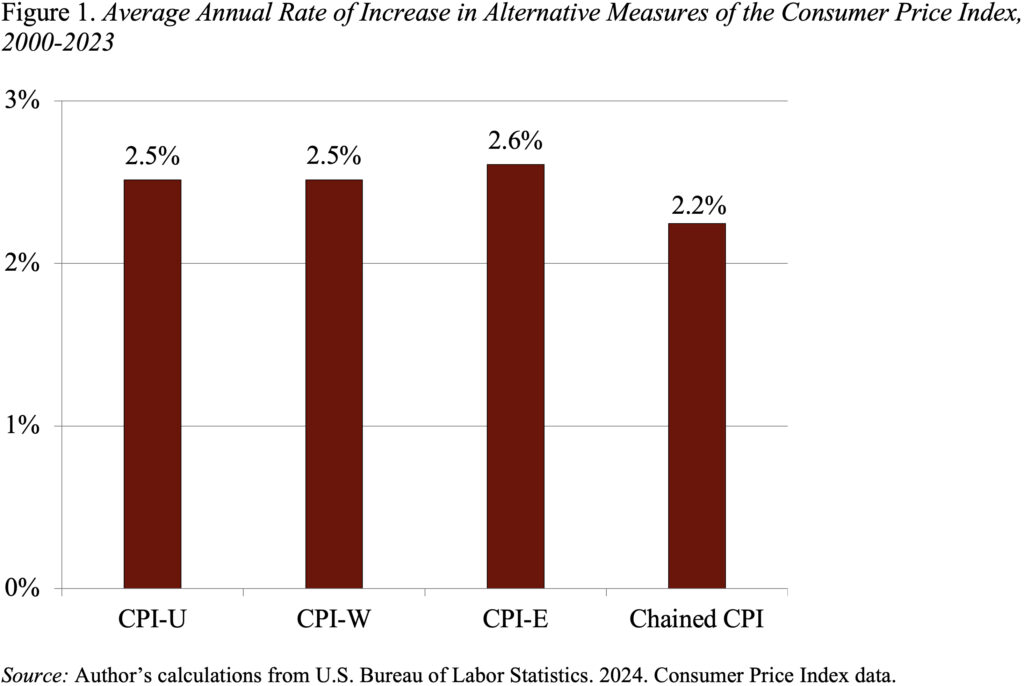

Desk 1 exhibits how every of those measures of client costs have modified between July 2023 and July 2024. As anticipated, the CPI-W and CPI-U are very shut (in truth, equivalent right here), the CPI-E rose sooner, and the chained CPI elevated extra slowly.

The identical sample is clear when trying on the identical indices over an extended interval (2000 – the primary yr for which “chained CPI” knowledge can be found – to 2023).

Shifting from the CPI-W to both the CPI-E or the chained CPI would have a noticeable impact on the price of Social Safety advantages over the subsequent 75 years. In calculating these results, this system’s actuaries assume that the CPI-E would improve the typical COLA by 0.2 share factors and that the chained CPI would cut back the typical COLA by 0.3 share factors. The projections present that transferring to the CPI-E would improve the 75-year deficit by 12 %, whereas shifting to the chained CPI would cut back the deficit by 17 %.

One might argue that each the CPI-E and the chained CPI would offer a extra correct measure of the inflation confronted by retirees. Thus, if we had been beginning with a value index that correctly mirrored the spending patterns of the aged, then transferring to a chained CPI may enhance accuracy. (Though some specialists query whether or not low-income aged stay too near subsistence to vary what they purchase in response to cost adjustments.) However on condition that we aren’t beginning with the proper measure, the case for switching to a chained CPI is weak. In view of the offsetting results – a 0.3 % overstatement of inflation resulting from not accounting for the substitution impact and the projected 0.2 % understatement resulting from not reflecting the spending patterns of the aged – the present technique of adjusting advantages appears nearly proper.