{kind=link}

The temporary’s key findings are:

- To encourage small companies to undertake retirement plans, policymakers have made it simpler to take part in A number of Employer Plans (MEPs).

- MEPs contain much less administrative burden and fiduciary duties than a stand-alone plan, and – in idea – might be cheaper.

- However few companies find out about MEPs, some fiduciary duties stay, exiting a MEP could also be tough, and MEPs could make mergers and acquisitions more durable.

- Additionally, it’s not clear that they do value much less, and any such evaluation ought to take into account worker – in addition to employer – charges.

- General, whereas MEPs might be enticing, adoption could also be sluggish on account of unfamiliarity with the product and uncertainty over any value benefit.

Introduction

At any given time, solely about half of U.S. personal sector employees are coated by an employer-sponsored retirement plan. Because of this, roughly one-third of households find yourself fully reliant on Social Safety at retirement, whereas others transfer out and in of protection all through their careers and find yourself with solely modest balances in a 401(okay) account.

The dearth of constant protection – a urgent concern for the nation’s retirement earnings safety – is pushed by small employers. Solely about half of small employers (these with fewer than 100 staff) supply a retirement plan in comparison with about 90 p.c of huge employers. In an effort to decrease the price of plans for small employers and thereby enhance protection, the SECURE Act of 2019 made A number of Employer Plans (MEPs) much less restrictive and probably extra enticing for this group. This temporary, which is predicated on a current research, explores each the probabilities and the constraints of MEPs in bettering protection in employer-sponsored retirement plans.

The dialogue proceeds as follows. The primary part gives a short historical past of MEPs and the creation of a much less restrictive subgroup of MEPs, referred to as Pooled Employer Plans (PEPs). The second part discusses the attainable benefits of PEPs for small employers, and the third part discusses components that will restrict their adoption. The ultimate part concludes that whereas PEPs might be enticing to small companies, employers could also be sluggish to undertake them.

A Transient Historical past of MEPs

Most retirement plans are sponsored and maintained by a single employer. The employer providing the plan is often the named fiduciary and should, in line with the Worker Retirement Earnings Safety Act of 1974 (ERISA), “run the plan solely in the interest of participants and beneficiaries.” Along with serving as a fiduciary, employers have to pick out a recordkeeper, make selections on plan design, file a Type 5500, and canopy the charges concerned in beginning and sustaining a plan. Managing all these duties could also be significantly difficult for small employers.

Not like single-employer plans, a MEP is a retirement plan adopted by two or extra employers and administered by a MEP sponsor. Though a MEP might be both an outlined profit or outlined contribution plan, the overwhelming majority are 401(okay)-type outlined contribution plans. By permitting employers to affix collectively to supply a plan, the MEP sponsor (sometimes a commerce or trade group or skilled employment group) takes on the fiduciary burden and spreads the executive, compliance, and value burden of providing a plan throughout a number of employers. Taking part employers in a MEP have their fiduciary accountability restricted to choice and oversight of the particular person or entity working their plan.

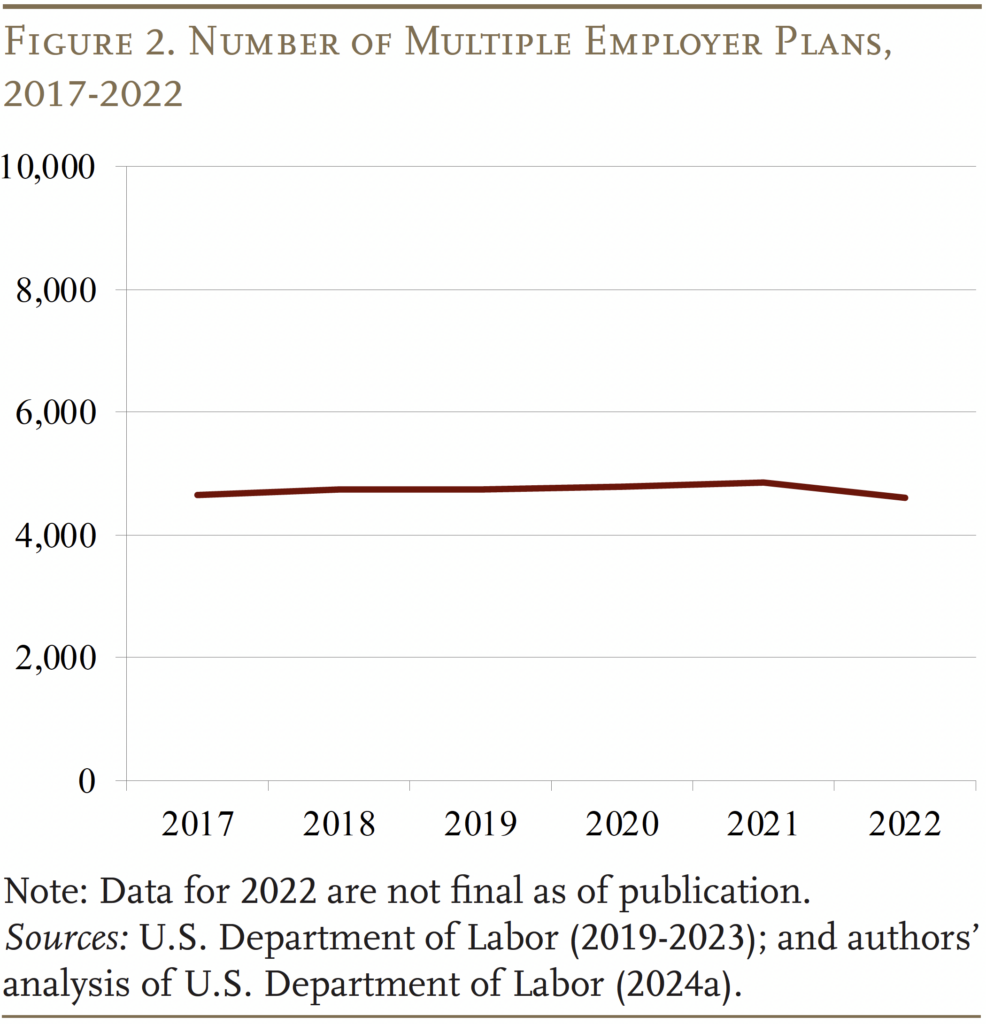

Whereas MEPs have been round for many years, they haven’t moved the needle on protection. In 2022, MEPs represented solely a sliver – 0.6 p.c – of whole personal sector retirement plans (see Determine 1), protecting about 6 p.c of energetic contributors.

Two predominant restrictions of MEPs could have restricted their adoption: 1) employers needed to share a typical bond; and a pair of) the entire MEP might lose its tax-qualified standing if one employer inside the group was not in compliance (the “bad apple” rule).

The SECURE Act of 2019 eliminated the “bad apple” restriction and created a brand new subclass of MEPs, referred to as PEPs, which aren’t restricted to employers with a typical bond. The laws stated that PEPs can solely be established by a pooled plan supplier (PPP), which takes on the position of named fiduciary and attends to plan administration, compliance, and auditing. PPPs must register with the U.S. Division of Labor (DOL) earlier than publicly advertising and marketing their providers and working a PEP. The extra regulatory necessities are designed to make sure that PEPs function in the perfect pursuits of staff.

The elimination of the widespread bond and unhealthy apple restrictions has generated a whole lot of pleasure, significantly amongst monetary providers companies, concerning the potential of those new plans to assist shut the protection hole. The newest DOL knowledge, nevertheless, present that preliminary take-up has been sluggish, with no important progress within the variety of MEPs because the passage of the SECURE Act (see Determine 2).

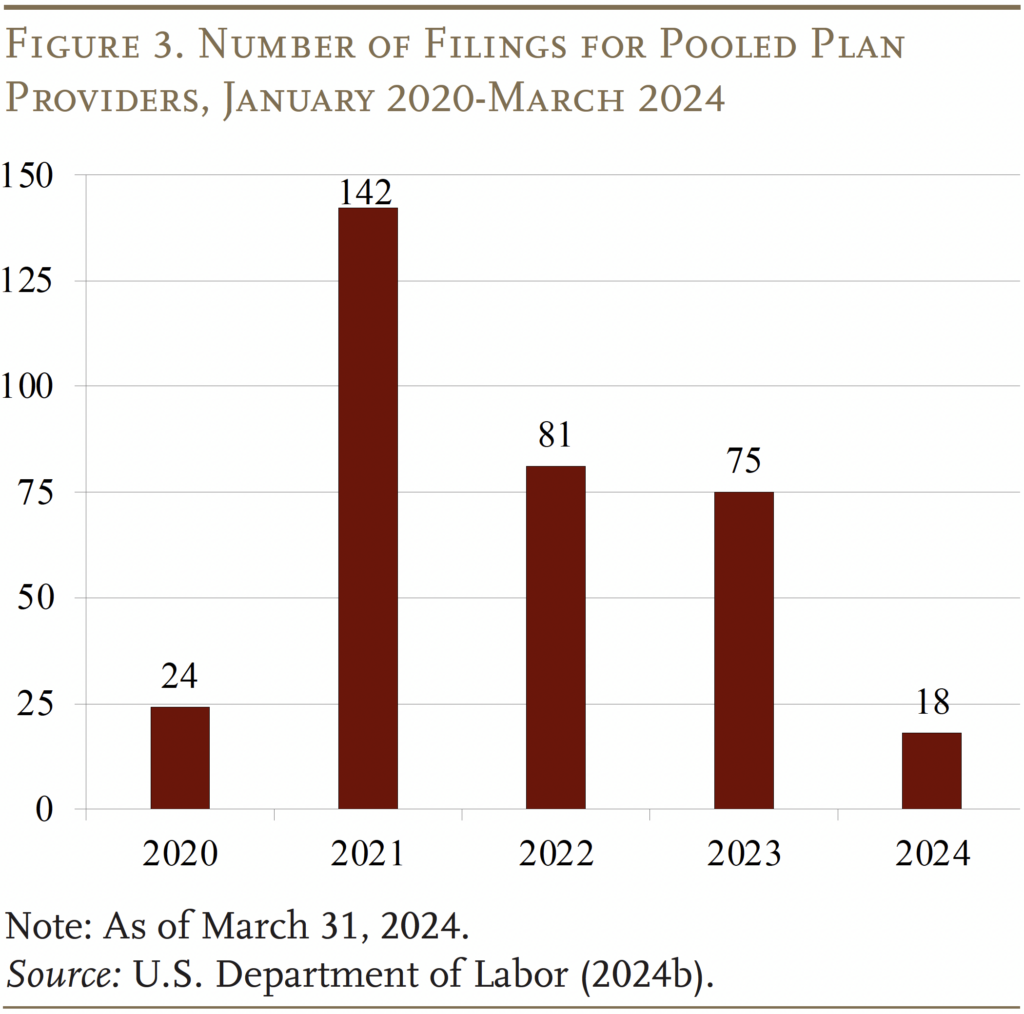

Furthermore, new PPP filings counsel that curiosity in PEPs could also be lower than anticipated. Whereas new filings climbed within the first 12 months after SECURE was handed, momentum slowed in 2022 and 2023 (see Determine 3). To get a way of the long run for PEPs, it’s helpful to contemplate their benefit relative to present choices for small employers and the way they might fall wanting expectations.

Doable Benefits of PEPs

The promoting factors for MEPs is that they provide benefits over present retirement merchandise for small companies and the potential for decrease prices.

PEPs versus Different Choices

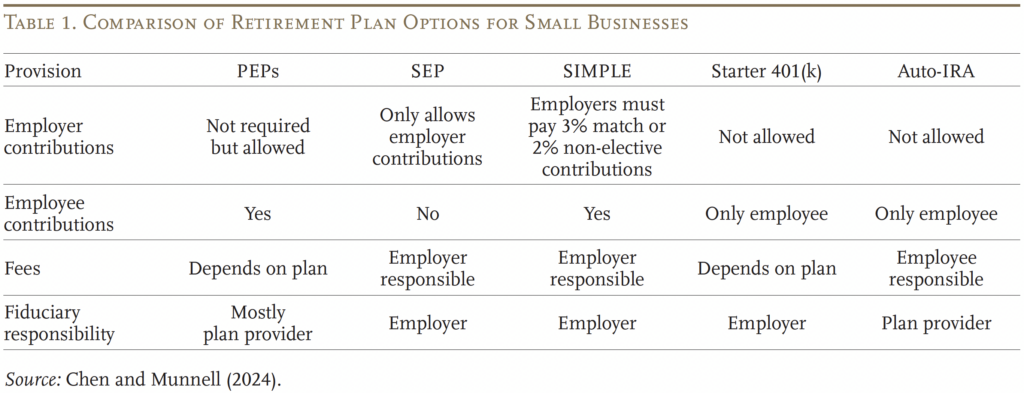

PEPs usually are not the primary retirement plan designed for small companies. Federal policymakers have tried for many years to increase retirement plan protection amongst small employers. Main initiatives embody the Simplified Worker Pension IRA (SEP) and the Financial savings Incentive Match Plans for Workers of Small Employers (SIMPLE). And SECURE 2.0 launched the starter 401(okay), another choice geared toward decreasing the prices of providing a retirement plan for small employers. Moreover, 16 states have launched or are making ready to launch applications requiring employers with no plan to mechanically enroll their staff in an Particular person Retirement Account (“Auto-IRAs”).

Desk 1 compares the traits of PEPs to the provisions of present choices. Not like SEP/SIMPLE plans, PEPs don’t require employer contributions, enable the sharing of the fastened prices of building a plan, and outsource the collection of the fund menu to a PEP administrator. Compared to Starter 401(okay)s, PEPs enable employers to outsource a lot of the fiduciary and administrative burden, get pleasure from decrease funding charges by aggregating belongings throughout extra employers, and allow employers to contribute. The principle benefits of PEPs relative to Auto-IRAs is that they’re obtainable in each state, 401(okay)s have greater annual contribution ranges than IRAs, and employers are allowed to contribute. Briefly, employers would possibly discover PEPs extra enticing than present choices as a result of they restrict fiduciary accountability, whereas sustaining the flexibility to pick out the supplier of selection and supply employer matches. The most important push for PEPs, nevertheless, has centered on prices.

Doable Value Financial savings of PEPs

PEPs promote value financial savings because of the economies of scale related to bringing collectively numerous small employers. Whereas two current research appear to contradict this competition, the outcomes do probably not mirror an apples-to-apples comparability. The research, utilizing MEPs knowledge from earlier than the SECURE Act, discovered that MEPs have been at the very least as costly, if no more costly, than single-employer plans of a comparable measurement. That discovering isn’t a surprise, given {that a} MEP with $10 million in belongings from 100 employers is inherently extra advanced than a single-employer plan with $10 million. The related query is how the typical value of a MEP with $10 million from 100 employers compares to the price of a single-employer plan with $100,000. These knowledge usually are not at the moment obtainable.

What the info do present is that the majority MEPs are fairly small – about 50 p.c maintain lower than $10 million and about 75 p.c have beneath 100 contributors. And small plans are dearer than giant ones. One research decided that at the very least 30 p.c of MEPs with lower than $10 million in belongings cost greater than 1.5 p.c for mixed administrative and funding charges.

Going ahead, it might be attainable that the expansion in PPPs will promote decrease charges on account of extra competitors and higher-quality funding merchandise. It may be, nevertheless, that employers with weak bonds to at least one one other pay much less consideration to plan prices. In reality, one of many two research cited above discovered that, amongst various kinds of MEPs, whole expense ratios have been greater for Skilled Employment Organizations MEPs, which have weaker employer bonds, than for affiliation MEPs or company MEPs, which have stronger bonds. If the PEP market develops like its guardian MEPs, it’s not clear that PEPs might be cheaper than single-employer plans – particularly given the expansion in low-cost 401(okay) plan choices for small employers. If PEPs usually are not cheaper, their solely predominant profit might be much less fiduciary accountability.

One other value consideration is how the charges are break up between the employer and worker, significantly for small plans the place charges are typically greater. Some PEP sponsors promote plans which have minimal charges for employers. Nonetheless, retirement plans usually are not free. Plans which can be free (or nearly free) to the employer should invariably cross on prices to plan contributors. If greater prices are handed on to staff, the query turns into how a lot greater are worker charges relative to single-employer plans? If worker prices are solely barely greater than stand-alone plans, PEPs might nonetheless be useful in serving to employees who would in any other case not have entry to a plan save for retirement. But when prices are considerably greater, PEPs might erode retirement financial savings for essentially the most susceptible employees and expose employers to extreme payment lawsuits.

Elements that May Restrict Adoption of PEPs

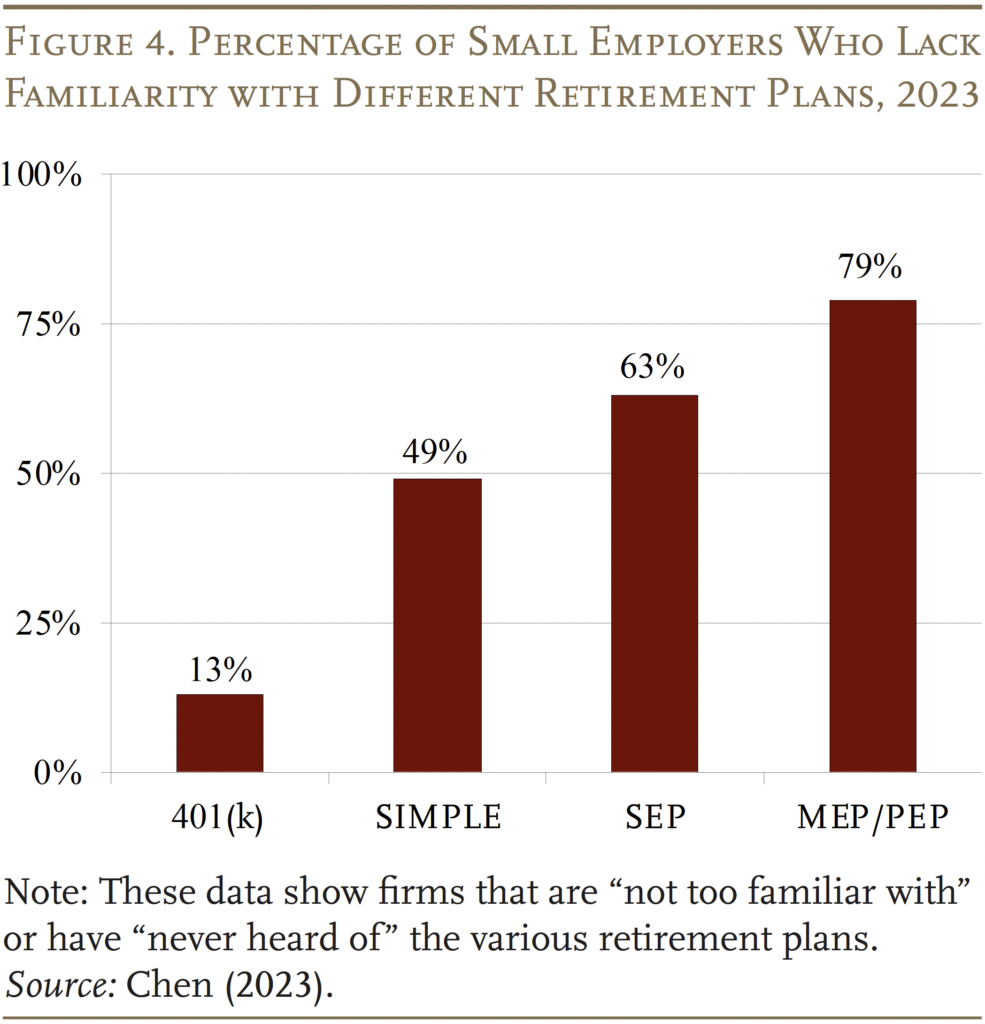

Numerous components might restrict the adoption of PEPs. The most important limitation of PEPs stands out as the lack of information. The overwhelming majority of small employers has by no means heard of PEPs or their guardian, MEPs (see Determine 4). PEPs, like all retirement plans, must be “sold” to employers – i.e., employers don’t come in search of them. Suppliers won’t solely must persuade employers that providing a retirement plan is efficacious, however that becoming a member of a PEP is the correct possibility for them. This problem is perhaps a excessive hurdle to clear.

Even when suppliers might overcome the notice hurdle, quite a few points stay.

- Value benefit could not materialize. As famous above, MEPs could prove to not have a value benefit for 2 causes. First, it could be arduous to beat the price of offering a single-employer plan, which has declined dramatically. Second, elevated competitors within the MEPs market might promote decrease charges, however employers with weak bonds might additionally pay much less consideration to plan prices. Lastly, plans which can be free (or nearly free) to the employers invariably cross on prices to plan contributors.

- Employer retains some fiduciary duties. Whereas the PPP is the named fiduciary for a PEP, the employer is accountable for choosing the correct supplier, monitoring the charges, and figuring out whether or not the providers provided are useful.

- Exiting could also be tough. An employer that will get larger and desires to transform to a extra customizable single-employer 401(okay) could discover it tough and time-consuming to terminate its portion of the PEP.

- PEPs may also make mergers and acquisitions more difficult. Whether or not an employer desires to merge its plan with a purchaser’s plan or fold an acquired employer’s plan into its personal plan, the method is way simpler with a single-employer plan.

Clearly widespread adoption of PEPs faces a whole lot of hurdles; solely time will inform whether or not this much less restrictive model of MEPs makes a dent in protection.

Conclusion

The dearth of constant protection is a urgent concern for the nation’s retirement earnings safety, and the protection hole is pushed by small employers. The unique SECURE Act created PEPs, a subclass of MEPs which can be much less restrictive and probably extra enticing for small employers. Whereas PEPs supply a number of advantages – equivalent to potential economies of scale and restricted administrative and fiduciary duties – small employers could also be sluggish to affix PEPs. They’re an unfamiliar product, and it’s not clear that they may have a value benefit over stand-alone plans for small employers.

References

Biggs, Andrew G., Alicia H. Munnell, and Anqi Chen. 2019. “Why Are 401(k)/IRA Balances Substantially Below Potential?” Working Paper 2019-14. Chestnut Hill, MA: Heart for Retirement Analysis at Boston Faculty.

BrightScope and Funding Firm Institute. 2023. The BrightScope/ICI Outlined Contribution Plan Profile: A Shut Take a look at 401(okay) Plans, 2020. San Diego, CA: BrightScope and Washington, DC: Funding Firm Institute.

Chen, Anqi. 2023. “Small Business Retirement Plans: The Importance of Employer Perceptions of Benefits and Costs.” Particular Report. Chestnut Hill, MA: Heart for Retirement Analysis at Boston Faculty.

Chen, Anqi and Alicia H. Munnell. 2024. “A Multiple Employer Plans Primer: Exploring Their Potential to Close the Coverage Gap.” Chestnut Hill, MA: Heart for Retirement Analysis at Boston Faculty.

Mitchell, Lia and Aron Szapiro. 2020. “Paperwork or Panacea.” Chicago, IL: Morningstar Coverage Analysis.

Shnitser, Natalya. 2020 “Are Two Employers Better than One? An Empirical Assessment of Multiple-Employer Retirement Plans.” Journal of Company Regulation 45: 743.

U.S. Division of Labor. 2019-2023. Non-public Pension Plan Bulletin. Washington, DC.

U.S. Division of Labor. 2024a. 2022 Type 5500 Datasets. Washington, DC.

U.S. Division of Labor. 2024b. Type PR Registration Filings Search. Washington, DC.