{kind=link}

Affect depends upon sources of earnings, asset holdings, and the quantity of fixed-rate debt.

In June 2022, U.S. inflation peaked at 8.9 % – a dramatically excessive stage after practically three a long time of comparatively secure costs. A shock of this magnitude should certainly have affected the retirement safety of close to retirees and retirees. The query is which teams and by how a lot.

As a result of it’s onerous to evaluate the influence of right this moment’s inflation shock from previous expertise, my colleagues Laura Quinby and JP Aubry mission the funds of six hypothetical households – of various ages and wealth ranges – below completely different doable financial situations. They had been fascinated about two outcomes (in comparison with a no-inflation state of affairs) – the cumulative change in actual consumption from 2021 to 2025 and wealth in 2025.

Analysis to this point reveals that inflation impacts households in a different way based mostly on the particular sources of their earnings, the allocation of their belongings, and their publicity to fixed-rate mortgage debt.

- On the earnings aspect, since wages and salaries are sometimes negotiated yearly, earnings are likely to lag inflation. And unemployment poses a major danger if the Federal Reserve’s response to inflation triggers a recession. Equally, many retirees nonetheless depend on outlined profit pensions, which frequently don’t preserve tempo with inflation. On a extra optimistic be aware, most retirees additionally obtain totally inflation-indexed earnings from Social Safety.

- On the wealth aspect, monetary fashions predict that bonds and different fixed-income holdings endure from sudden value will increase, whereas equities fare higher, as long as the Federal Reserve avoids a recession. And whereas home costs rise with inflation, this progress could also be offset by shrinking demand if mortgage charges rise. Alternatively, households that already maintain fixed-rate mortgage debt profit from inflation as a result of the month-to-month mortgage cost stays fixed at the same time as family earnings rises with costs.

The state of affairs evaluation includes making use of the consequences described above to the earnings and belongings of a pattern of near-retiree and retiree households from the Survey of Client Funds. In each instances, the situations mimic the precise financial system from 2021 to 2023 after which diverge as follows:

- Tender touchdown: After 2023, the financial system is on a clean path to 2-percent inflation, the output hole closes, and the Federal Funds Price drops to 4 % by December 2025.

- Recession: After 2023, inflation begins to rise once more, and the Fed responds aggressively – triggering a recession and a decline in inflation. In response, the Fed shortly brings charges again down; nonetheless, the financial system doesn’t totally recuperate by 2025 – the tip of the evaluation interval.

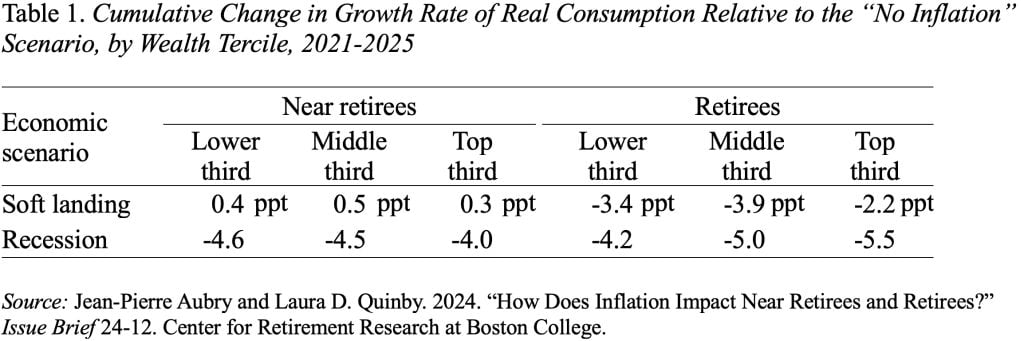

The outcomes – in comparison with a no-inflation state of affairs – are fairly fascinating. When it comes to the change in actual consumption, two factors stand out (see Desk 1). First, close to retirees expertise a smaller decline in consumption than retirees as a result of they maintain loads of fixed-rate mortgage debt.

Retirees have much less erosion of actual debt, and infrequently additionally lose actual earnings as a result of pension advantages are solely partially listed to inflation. Second, the influence of inflation varies throughout the wealth distribution.

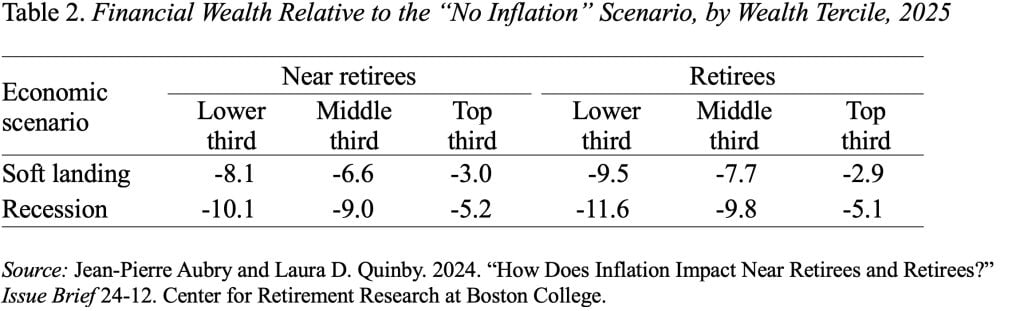

When it comes to monetary wealth in 2025, inflation has an unambiguous unfavourable influence (see Desk 2). Prime-wealth households, nonetheless, at all times lose lower than their lower-wealth counterparts, as a result of they make investments extra in equities, companies, and different belongings that develop with inflation. (As anticipated, inflation doesn’t have a lot influence on housing wealth.)

In brief, experiencing a bout of excessive inflation later in life is mostly dangerous to retirement safety, however the influence varies relying on the extent to which earnings and belongings develop with (or lag) inflation, and the quantity of debt excellent.